Whats Up with Markets?

Whats Up with Markets?

We are supposed to be in the worst economic downturn since 2008, maybe worse. So, why are markets zooming higher?

There is real economic pain being faced by businesses and individuals. People have lost jobs, companies are cutting back, lots of uncertainty to go around. But markets seem to be operating in a different universe. Indices are up more than 30% from March lows and there is general optimism in the market in stark contrast with the bleak mood of people in the real economy. Why?

I think there has been never a better time to understand how markets work than this and here is our attempt to explain what’s been happening.

Markets are Forward Looking

I remember watching Bloomberg in Mid January and seeing that Asian markets were down sharply because of reports of a new SARS like virus. This was before the Wuhan lock-down, before it spread elsewhere and everything that followed. And as the virus spread, prior to governments and the public across the world acting, markets reacted. They were prescient, except that this is an essential functions of markets.

Markets are meant to discount all available information of future events. When the markets came down sharply, they were ‘pricing in’ lot of uncertainty about the lethality and contagion effects of the virus, governments response and economic impact. News predicted imminent apocalypse.

And then, we got to know a lot more about the virus. Central banks and governments opened the monetary and fiscal stimulus spigots. More than 100 different groups all over the world started working on vaccines and cures. And even with the virus still spreading more rapidly, the markets recovered sharply as it started discounting the future economic impact of the virus given all this new information and how conditions will be a year from now and longer.

Earnings Matter Most

All asset prices reflect the present value of future cash flows. Value of a commercial property, for instance, is a reflection of what someone is willing to pay today for all the rental income it will generate in it’s life-cycle and the residual value at the end of it.

A stock similarly reflects all the future free cash flow, i.e. earnings - adjustments for increase in working capital and capital expenditures, it will generate.

Stocks move up and down primarily because change in earnings expectation of companies.

The best example for this is when last year the Finance Minister announced India will reduce its corporate tax rate to 25% and markets quickly adjusted and moved up significantly before the day was over. This was market adjusting to the fact that lower tax rates would mean higher earnings, even if nothing else changes.

Risk Premium

Present value = future cash flows adjusted by a discount rate that reflects the risk free interest rate + liquidity + economic risks + sector and company risks + other uncertainties.

For example, if you were buying a commercial property today you are considering future rental payments against keeping the money safely in a bank, chances of future recessions, vacancy risk and tenant specific risks. There is lot of uncertainty to all those assumptions, so the rational way is to assign a probability of those outcomes and its impact and take that into account into today’s value of the property.

If interest rates rise, then stocks fall because it increases the discount rate. Or, if there is increased geopolitical tensions and stocks sell off, it’s because there is greater uncertainty and risk premiums climb up.

A sector like Pharmaceuticals has it own specific risks of regulatory actions that are unknown and therefore companies in that sector might have higher risk premiums. But within the sector, a company with a good track record of no adverse regulatory actions might have lower risk premiums than it’s peers, allowing it to trade at a much higher valuation.

Low Interest Rate Environment and Liquidity

Monetary policy which determines interest rates and liquidity play an important role. Lower interest rates increases the price of an asset because it reduces the discount rate. However, monetary policy also affects the demand for stocks.

Ever since the financial crisis of 2007-08, central banks globally have brought down interest rates to near zero and flooded the market with excess liquidity. So much so that trillions of dollars worth of bonds are yielding negative interest rates. Even in India, the Repo Rate, the rate that the central bank lends short term loans to banks is at a low of 4%.

When interest rates are low, it pushes the demand for riskier assets higher. For example, with 10 year bond’s yield at 0.25%, Nestle, with a 1% dividend yield and positive return expectation of 2% annualized appreciation, would be orders of magnitude more attractive than the long bond.

Since the financial crisis, central banks in the developed world have also continued to experiment with unconventional tools to support the economy by increasing liquidity in the system.

Let’s say I’m a really bad businessman. I borrowed $100 at 5% and invested in a project that is returning only 3%. In a different world, I would go bankrupt and my assets would be auctioned off. However, because of central bank actions, I can now borrow $200 at 1%, retire my old debts, buy back stock with the rest, and continue doing a bad job.

While low interest rates and high liquidity have helped steer the economy off a cliff, a lot of the liquidity has also found its way in to the market.

In India, the markets have also benefited from increasing fictionalization of the economy. Driven by demonetization, formalization and reduced interest in physical asset classes such as gold and real estate, more savings has poured in to financial markets in recent years and propped up the markets.

Price Multiples, Risk Premium and Sentiment

Many commentators judge whether a stock is cheap or expensive based on it’s price/earnings (PE) multiple. I would argue that solely judging a company based on this ratio is meaningless, the appropriate PE is based on many factors such as probability of certainty of future earnings and its growth, quality of management, competitive advantages and other tangible and intangible asses.

Also, risk premium and sentiment have considerable impact on price multiples. If interest rates are low, say at 0.25 %, and you have a stock at 40 times earnings, but a dividend yield of 1.5% and good visible economic prospects in the future, is that stock cheap or expensive?

If the general consensus based on economic indicators is bullish and stocks are trading at high multiplies, does that mean automatically stocks are expensive and one should simply shift out with no economic evidence for it and miss out on the likely upside, that does not seem rational.

Composition of the Market and Stock Indexes

Indices are not the market. The media often confuses between the two. But if you look at the National Stock Exchange, for example, there are over 1,500 stocks that trade every day. But the Nifty index has only the largest 50 stocks in it.

Larger companies have stronger ability to withstand a crisis since they have better resources and access to capital, products or services that are more entrenched with higher market share or barriers of entry and better positioned to lobby for favorable economic policies or squeeze employees or suppliers.

So, while some large market-cap stocks have rallied and pulled the indices up, they are not representative of the broad market.

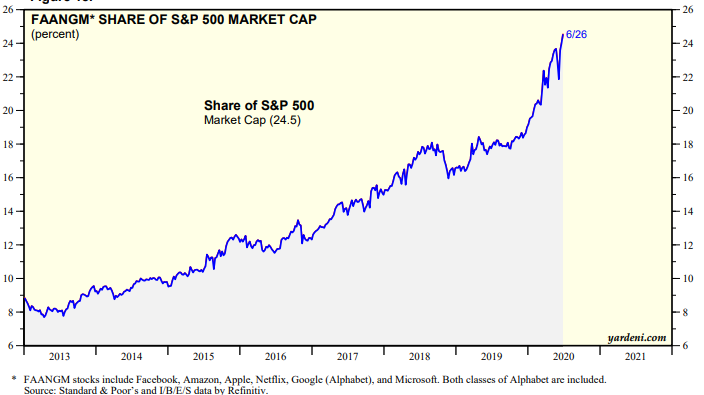

In this particular crisis, there has been another trend, especially in the US, technology companies which were already having a dream run before this, are again mostly in the green for the year. This is because of the belief that the trend to more digital world has been accelerated due to this crisis. Technology companies now constitute a large % of weightage of total value of S&P 500, like Facebook, Apple, Netflix, Google, Microsoft, Amazon and NVIDIA (FANGMAN) now have a combined total market cap of $ 6.7 trillion dollars, which is 25.1% of the S&P 500 total market cap compared to 15.7% at the end of last year. Therefore a large part of the recovery in stock prices is driven by these seven stocks alone.

The front-line stock indexes that we track and hear about in the media need not mirror the broader economy or the market as a whole - a few stocks or favored sectors can have a disproportionate influence on them.

Source: Yardeni Research

Putting it All Together

In summary, indices have being driven higher by companies that have benefited from this crisis or are guaranteed to survive and have better prospects in the future. It’s also being propped up significantly because of low interest rates and easy liquidity.

What will happen next?

Will the distortion between markets and real economy continue to persist or will it all coming crashing back down once liquidity starts to dry out or the economic fallout worsens. Or will the markets have signaled much ahead that the downturn was largely contrived due to the lock downs and once things go back to normal, it will come back stronger.

There are some good arguments on both sides. But what will happen exactly is hard to predict, especially if your time horizon is 2-3 years.

Markets are volatile because it’s always pricing in various uncertainties and more so in such an unprecedented situation.

So how should one invest?

Should you invest now or stay invested? If you do and markets move up from here, it’s all good. However, if they fall and you lose money, you would regret especially because, in hindsight, it would be like the economic dangers were obvious and the markets were too optimistic.

If you don’t invest and the markets subsequently move up, you will experience the fear of missing out (FOMO) and regret it. But if the market falls, because you stayed in the sidelines, it will make you feel smart.

So what should one do? how does someone navigate this maze? We answer this next week.

Another insightful article. Eagerly waiting for the next week's issue