Money Printing and Markets

Money Printing and Markets

In the coming years, the most important influence on markets is most likely going to be the changing role of monetary policy

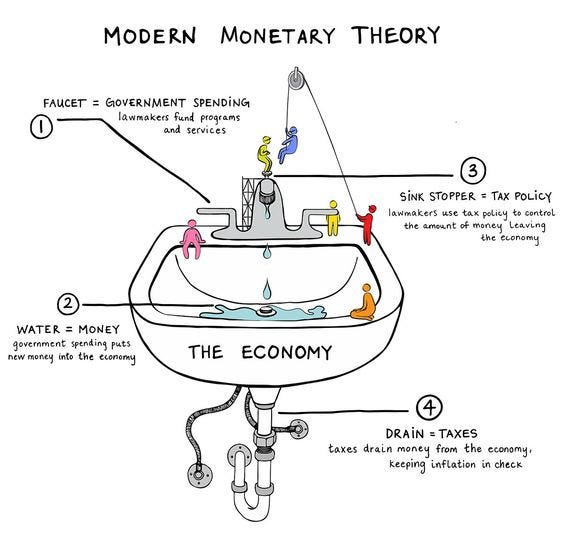

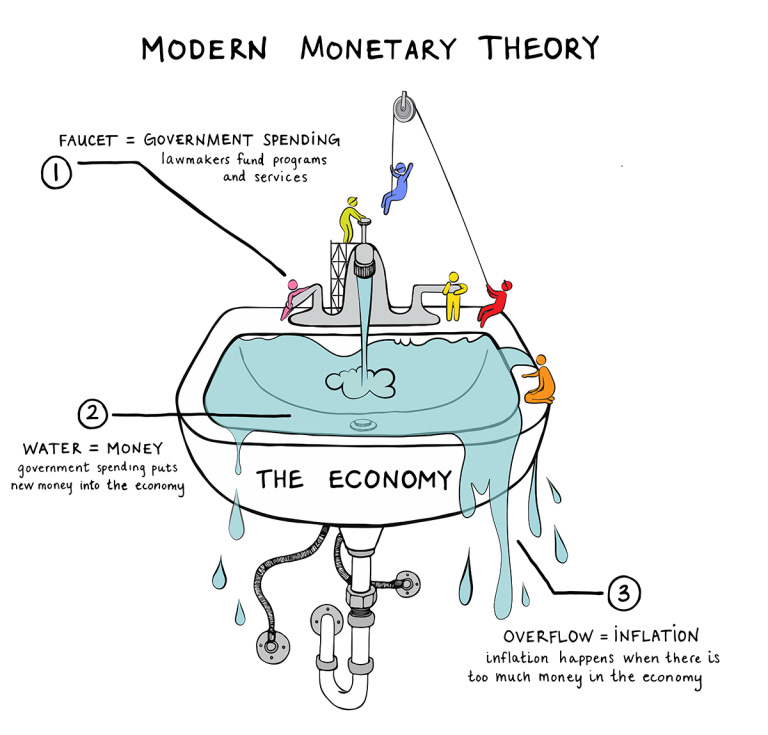

Source: https://www.marketplace.org/2019/01/24/modern-monetary-theory-explained/

If first half of 20th century was dominated by wars, this century’s first half major influence will be monetary policy.

Ever since the financial crisis of 2008, central banks have expanded their toolbox and responded in unconventional ways such as reducing interest rates for long periods to 0% (ZIRP,) embarked on measures such as Quantitative Easing (QE) which is purchase of government and non-government debt, even equities in case of Japan and some even experimented with negative interest rates (NIRP.) All this in pursuit of increasing money supply to stimulate economic growth.

The unconventional theory that will dominate monetary discussions is the concept of Modern Monetary Theory (MMT).

Without going deep into esoteric aspects of monetary economics, MMT basically states that a ‘sovereign’ is not a household that needs to care about balancing its budget. A country that prints its own currency can never run out of money because it can simply print more and finance it’s own spending without raising additional funds via taxes or market borrowing.

This process has accelerated in recent years for two reasons:

Social programs: The central banks ability to stimulate the economy by creating money supply has not gone unnoticed by advocates that want to expand social programs such as free college, healthcare coverage, combating climate change and others. The argument goes that the country is more than its economy and deficit spending does not matter anymore, and therefore it does not make sense for a country to allow its citizens to suffer unnecessarily in pursuit of an abstract idea of keeping deficits in check.

Corona crisis: This particular crisis is unique because it’s entirely been government induced. The true black swan event of 2020 has not been the virus but the almost global lock-downs that has pushed economies to witness a major drop in GDP that is unparalleled in economic history. This drop in GDP has led to fall in government tax revenues but also has forced government to increase its own spending to support businesses and citizens who have been asked to stay home. So government spending in this period in developed and even emerging markets has been financed by increased government borrowings including by itself or central bank buying its own bonds.

Now that the dam has been broken, there will be more demands to expand the use of MMT.

The question most people will have is that, we have been told that government simply printing money leads to inflation, which is textbook but the world is more interesting:

There is lot of academic and actual experience that has shown that in developed countries that MMT instead of inflation actually causes deflation. There are many theories to why such as developed countries have a more efficient economy, aging population, easy and low cost of funds reduces productivity because there is no longer a push to complete a project in time. Also that conventional major economic stimulants such as infrastructure is mostly already built in most developed countries, so MMT produces diminishing returns.

Japan has embarked on QE or MMT for more than 20 years now and has not seen inflation spike. Europe has seen 0% or negative interest rates for 10 years now and European central bank has used QE for as long and inflation has been subdued. So there is some truth to this story.

The true difference between emerging markets and developed countries might turn out to be this. If India or Brazil experimented with MMT, inflation will surely spike up, limiting the effects of MMT. However, this will not prevent emerging countries from experimenting with it. So we can assume that this will be the trend in the near future.

So till inflation roars, this party will go on.

And this, will have a profound influence on markets. It’s already had, most commentators will cite this as number one reason why markets have rallied so sharply from their March lows even though most economies are in doldrums.

Here are some aspects of how this will impact markets and economies in the near future:

Value: For example, take a town of 100 people with 3 stores in it which are grocery, entertainment and alcohol. Assume that the government gives all the 100 people, every month 1000 rupees each. All the 100 people will go spending their money in those 3 stores. So every month that money flows to those 3 stores, so even though the government is providing income support to the people, cash is flowing to the businesses that are actually providing value. It’s productivity that creates wealth. So economic inequality will worsen but for markets, businesses in general should prospects look brighter because they create value.

Startups: One of the consequences of this unconventional monetary policy has been that it’s become easier to start companies that are able to scale rapidly and achieve dominance in a very short period period of time. This has been achieved with young companies able to raise funds to finance their ambitious growth without looking at profitability in the short. First objective has become to grow fast, acquire customers and their mind-share and capture market share. This has been facilitated to an extent because of easier monetary policy. And as MMT expands, there will be more venture capital and private equity funding out there due to first and second order effects and there will be more disruptions.

Money supply: The purpose of MMT or QE was to stimulate the economy by incentivizing banks to lend, rather what it’s done is that it’s helped keep the markets afloat. Increased money supply normally benefits markets because there is more money out there and instead of it going to illiquid assets such as real estate, it usually ends up finding its way into markets. Also, increased money supply reduces the attractiveness of fixed income because it forced yields much lower and increased the demand for high quality equities, even if it looks expensive.

Shocks: There will be a general belief among market participants that whenever the next crisis hits that the central banks and other policymakers will be forced to act like they have done in order to support the economy but also ends up propping up the market by distorting it. The pressure from the markets will grow more profound and consequences of central banks not stepping in will be worse at that stage.

So a rational way of looking at markets right now will be:

Stocks especially companies that are growing fast or high quality will outperform. There used to be a tendency to think that stocks above a certain P/E was expensive but i think with low interest regime and low money supply, stocks with high visibility and decent dividend yield and positive capital appreciation expectations should do well.

For example, a stock like Infosys might grow in low single digits in the next decade but if there is strong visibility of earnings and dividend yield is at 2%, then there will be lot of buyers for the stock especially institutions or individuals globally will look at high quality companies in lieu of government or high quality corporate debt which has negative or really low interest rates.

So stocks that are considered defensives like pharmaceuticals or consumer brands or ones that are still growing with strong competitive advantages such as Asian Paints or Apple with strong outlook that in 2030 or 2040 these companies will be still around and growing, will not only stay expensive in relative terms but will continue to outperform.

If one has an investment horizon of more than 3 years, it’s better to be in stocks or real estate than fixed income because this push for QE or MMT is here to stay. If it does backfire and lead to much higher inflation, then stocks and real estate will at-least appreciate nominally and if it does not, then the push for more monetary policy based funding will grow even stronger.

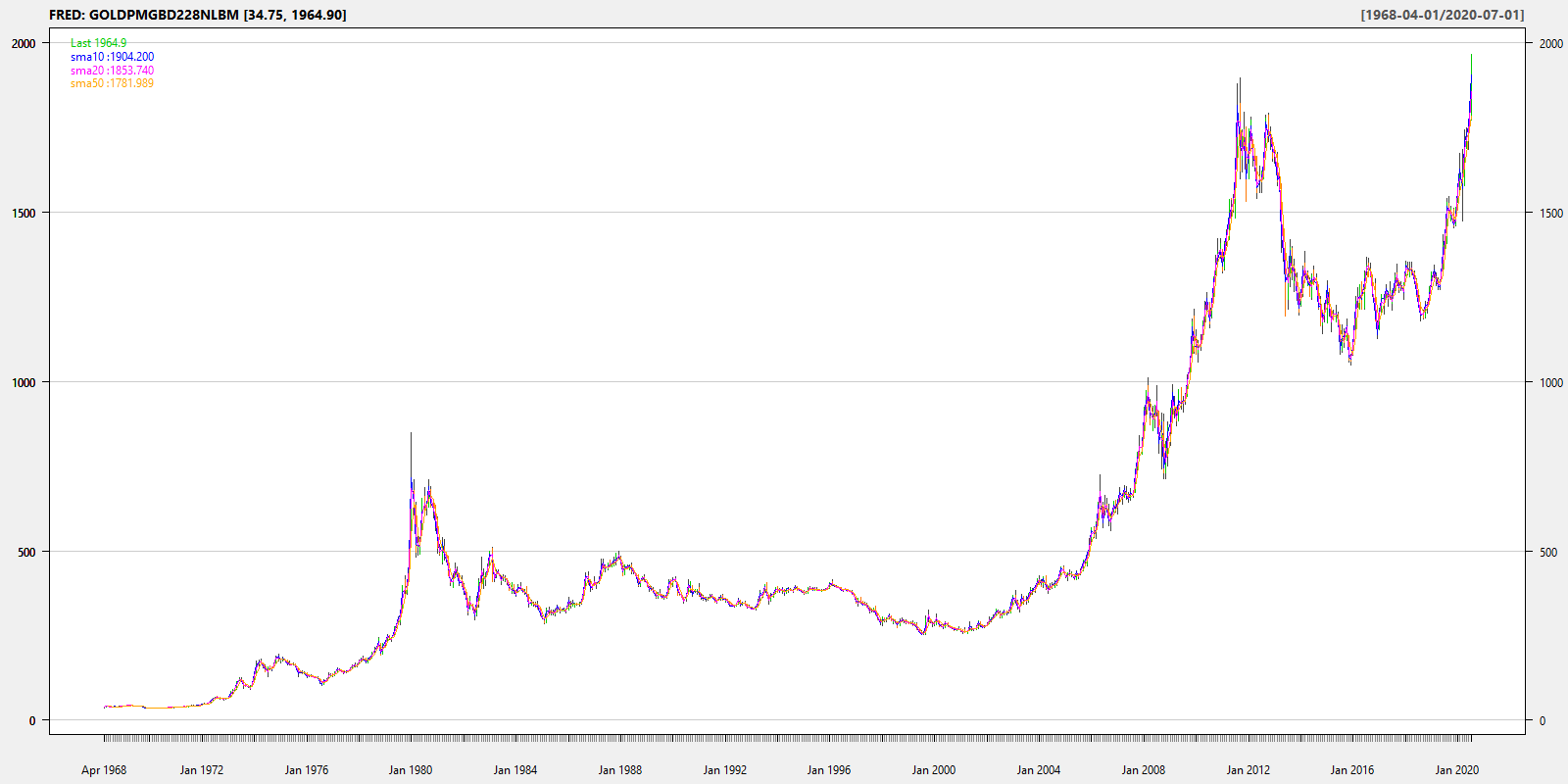

Gold has done really well in the past year and this is for three reasons, one because of higher tensions between US and China, a dystopian world the pandemic might produce and the expansionary monetary policy that is unprecedented. Gold traditionally acts a safe haven during crisis but also is a hedge against inflation and fiat currencies, while we are not like to go back to the gold standard but if inflation really comes back at some-point then gold is an interesting alternative asset class to have exposure to. Gold is better than Bitcoin because it’s endured as a store of value and medium of exchange for thousands of years, Bitcoin will need to prove that.

Diversify globally, given that there are lot more interesting ideas and innovation that happens in US, Japan and other countries as an investment strategy it makes sense to invest in areas which are likely to see higher growth and more innovation since that’s where the thrust is.

So while we do not like to time the markets or predict where markets are headed in the short term especially. It’s important to take a step back and frame an investment strategy based on a broader macro outlook for a longer duration.

Therefore we conclude that look at stocks and real estate, do not look at it from a point of view of that this company is overvalued in terms of P/E in relative to the past. It’s better to stick to quality because those competitive advantages will become more entrenched.

Also except in areas of technology, healthcare and few companies that will be outliers, do not expect much capital appreciation either because we might be in a period of low economic growth despite all the money printing.

Source: https://www.marketplace.org/2019/01/24/modern-monetary-theory-explained/

We will leave you with a few charts. All in terms of USD.

Agri-commodities, since 2012

Gold, since 1968

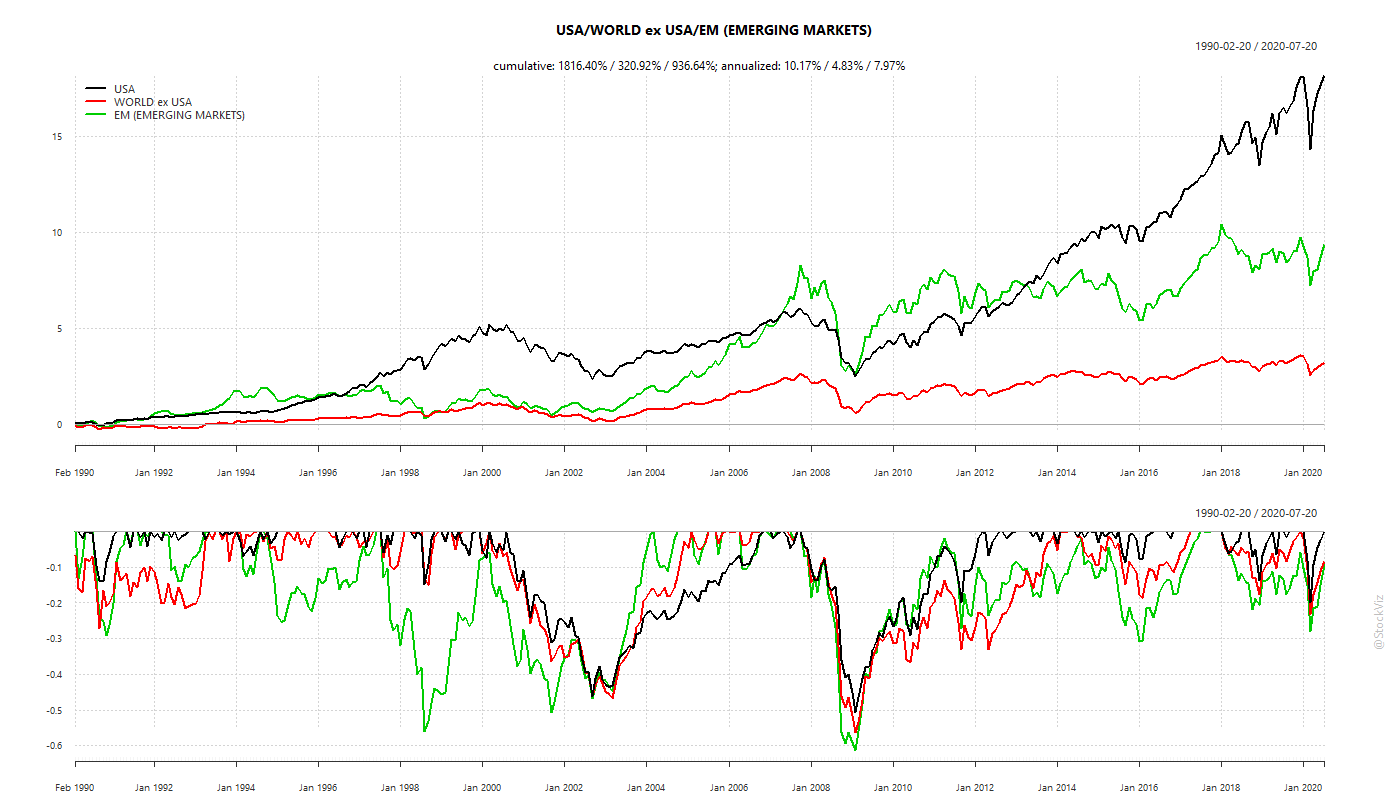

US vs. the rest, since 1990

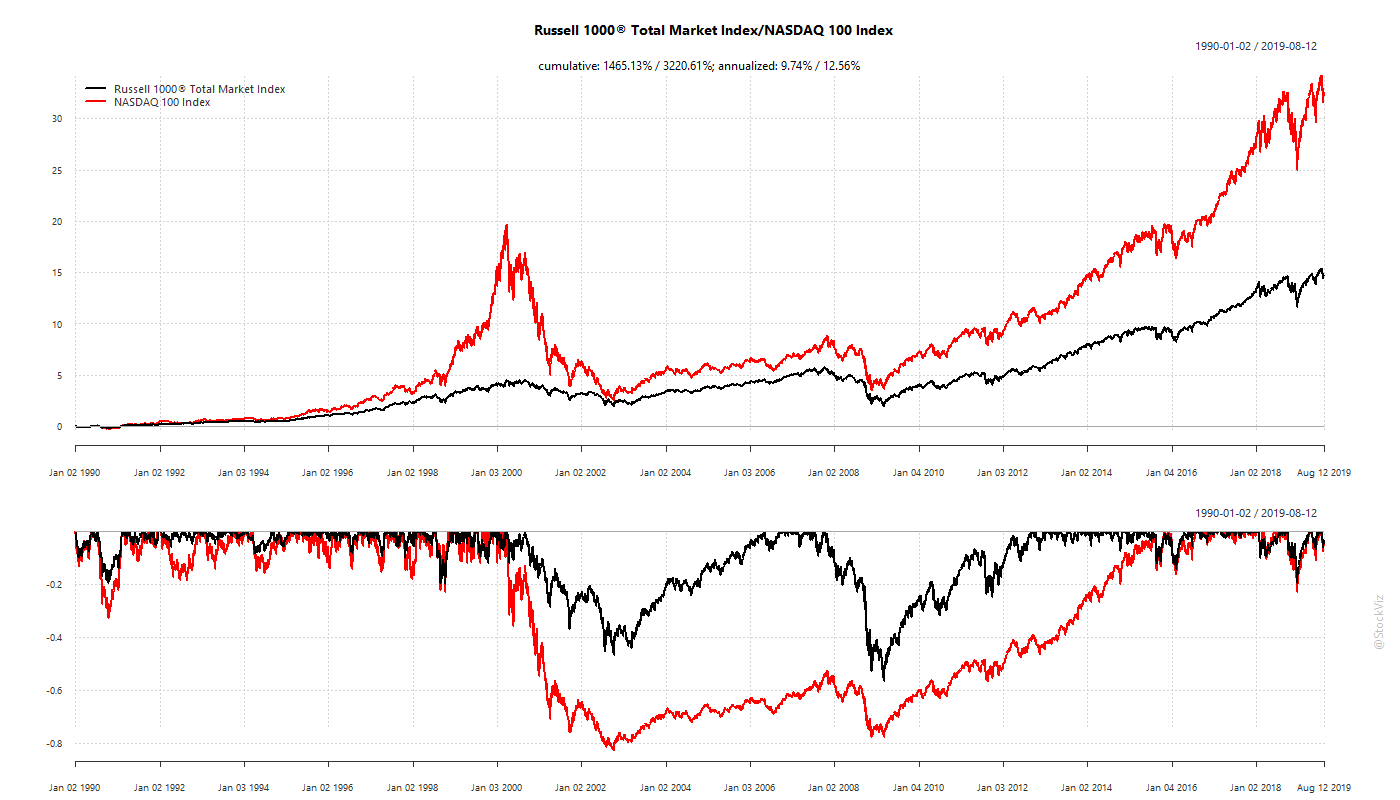

US Tech vs. US market, since 1990

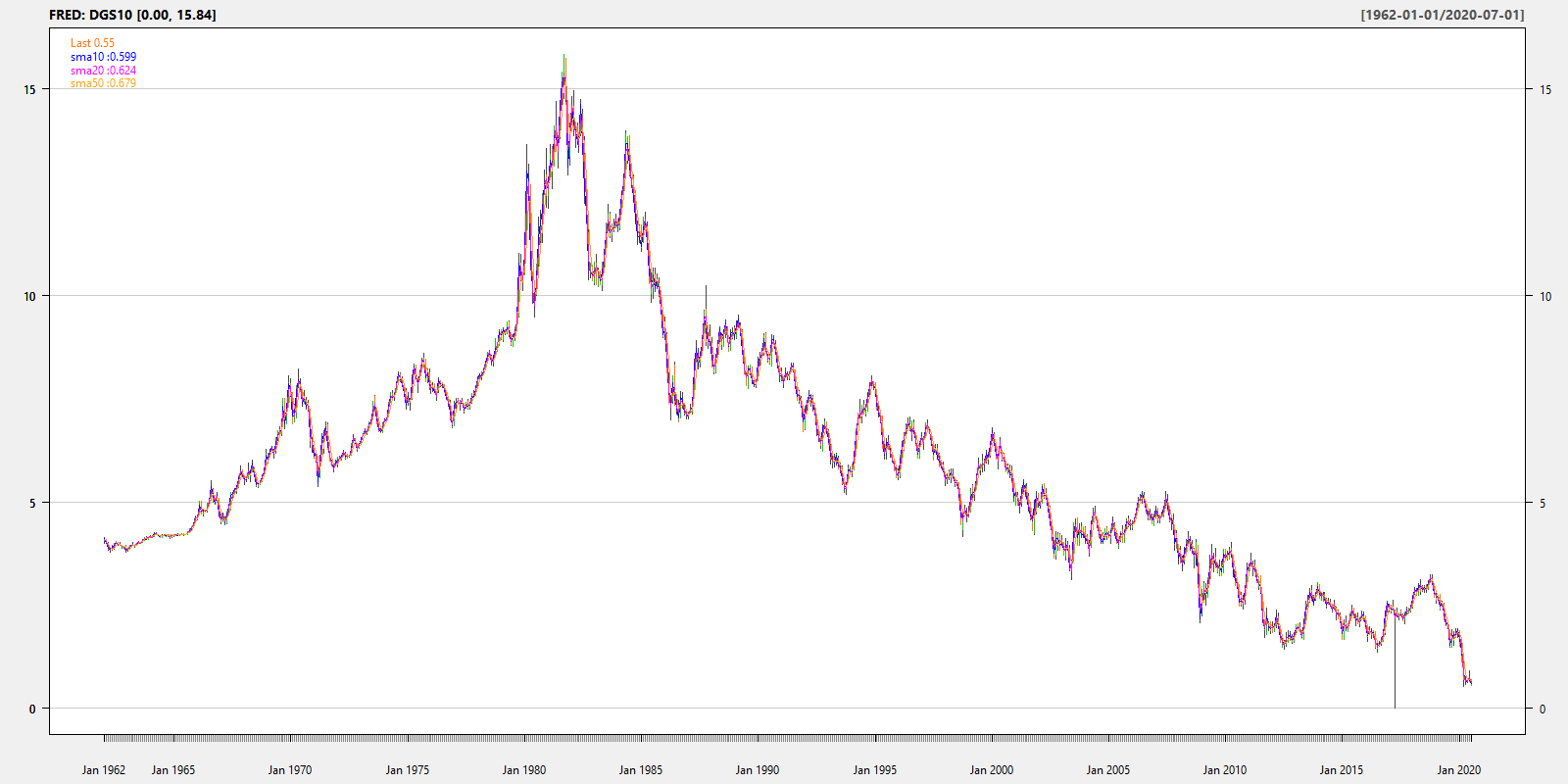

US 10-year bond yield, since 1962

Enjoy the discussion