When Buffett-heads are asked about when they are likely to sell a stock, they often bring out this quote from the Master:

A common-sense parsing of the actual quote would over-weight the “outstanding businesses” bit over “forever.” However, the quote has been deliberately misinterpreted by asset-managers (who are paid as a percentage of AUM) to keep investors tied into their funds in spite of extended periods of underperformance.

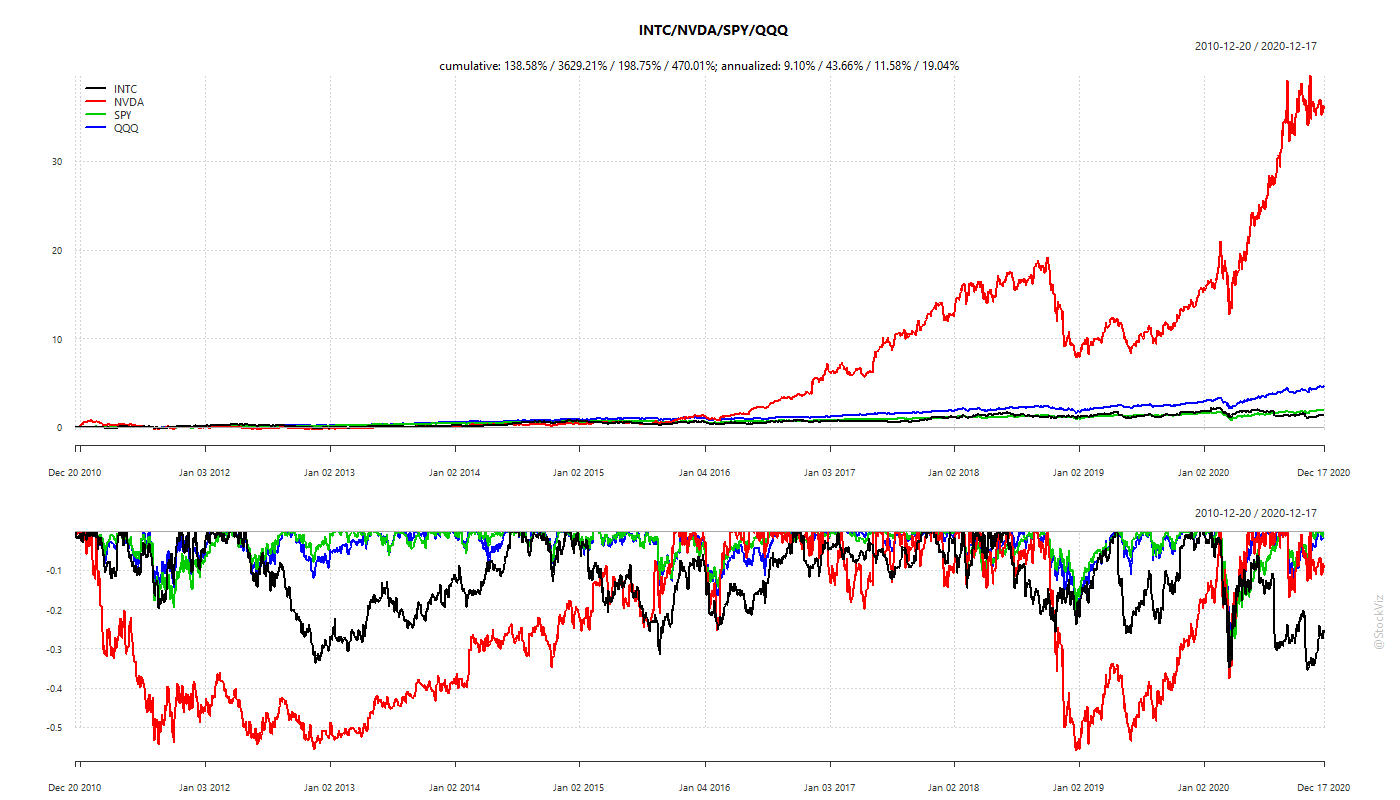

Corporate history is replete with examples of companies that once had the widest of moats but withered nonetheless. The most recent posterchild is Intel.

Over the last decade, Intel (INTC) trailed the broader S&P 500 and Nasdaq indices with the final death-blow being dealt by Nvidia.

Twenty years ago, could you imagine a world without Intel? Now you can. Apple, Samsung, Amazon, Google and Microsoft are all in the process of developing or have already developed processors to run their operating systems and power their data centers. For a deeper dive, read this excellent piece by James Allworth.

And it is not just hardware. Twenty years ago, could you have imagined that Infosys would beat IBM and the S&P 500? Yet, it did.

Oh! But that is tech, you might say. What about the “real” economy stocks?

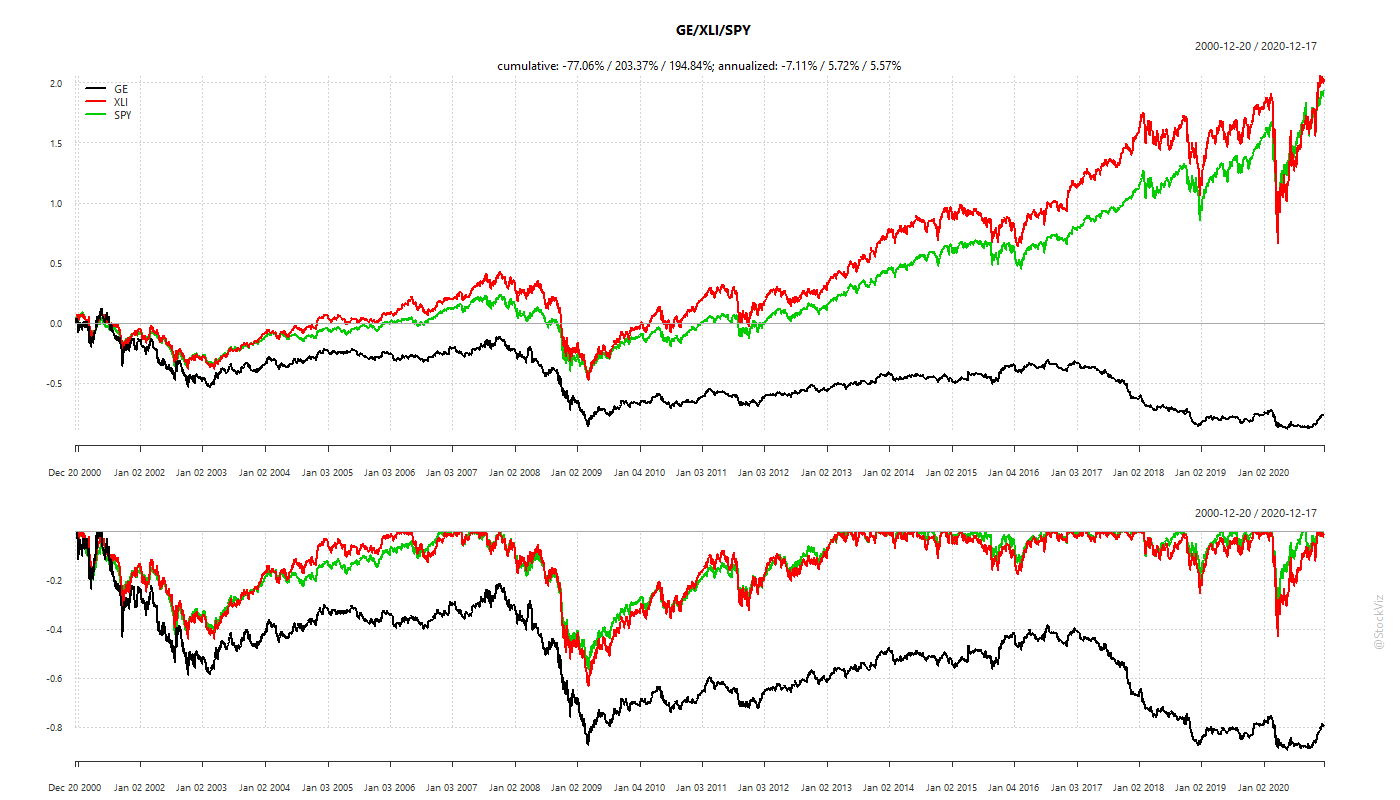

Remember GE? Their six-sigma blackbelts were supposed to be cream-of-the-crop problem-solvers who could be parachuted into any situation.

While you can argue that the above companies were cherry-picked, the base-rates are more shocking

A recent study by McKinsey found that the average life-span of companies listed in Standard & Poor's 500 was 61 years in 1958. Today, it is less than 18 years. McKinsey believes that, in 2027, 75% of the companies currently quoted on the S&P 500 will have disappeared. (IMD)

Often, experienced managers are experts at solving problems for an old world order. The “best” managements often miss creative destruction happening in their own backyard, like Kodak. Incentives typically are setup to reward reaching local maximas. So, it is entirely possible to hit every single quarterly number while steadily marching toward bankruptcy.

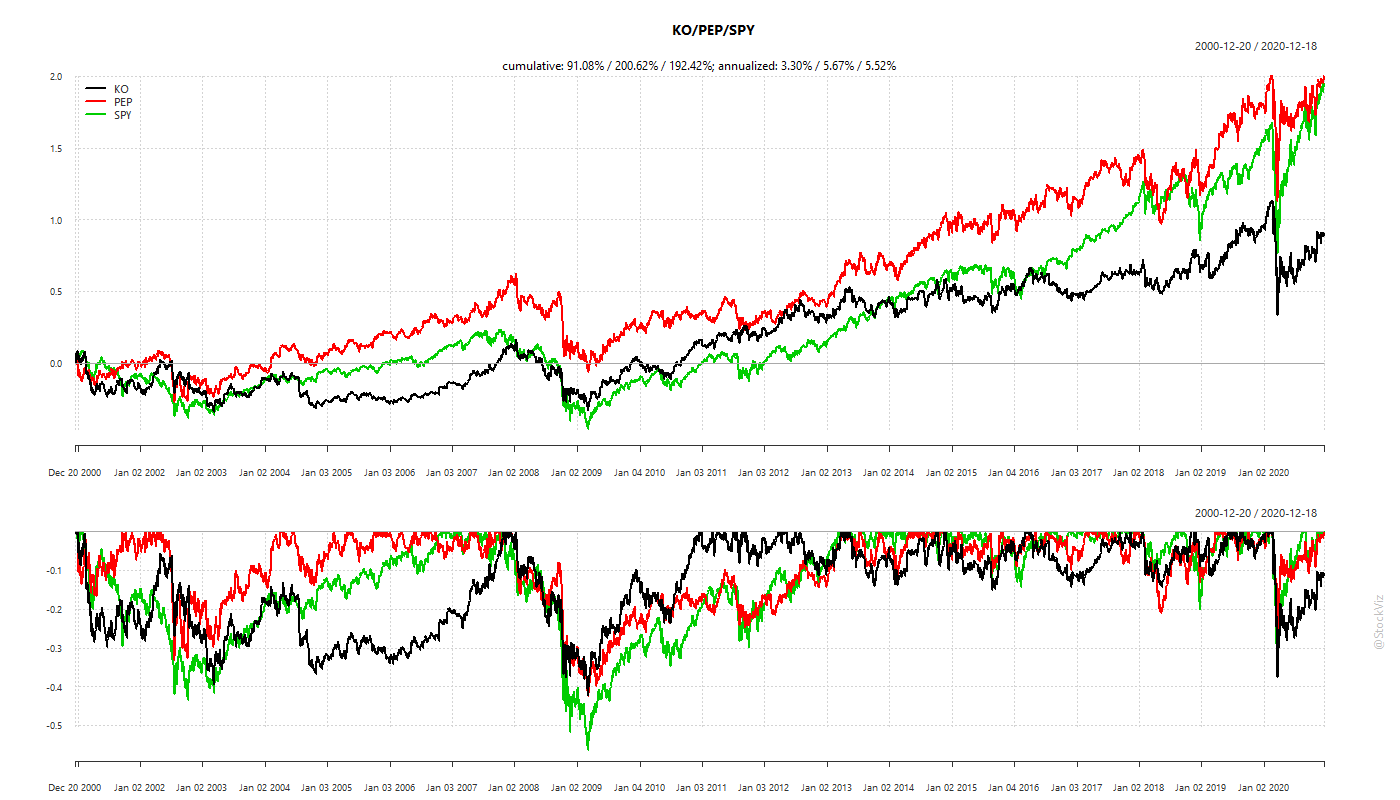

The Coca-Cola Company is an example where initial high expectations were merely met (and not exceeded) to the dismay of common-stock holders.

And what is true about individual companies it true about the broader market as well. A visit to Japan will blow your mind. But as an investment?

In fact, a simulation of historical country-index returns show that only DENMARK, USA and SWITZERLAND had an extremely small chance of posting negative buy-and-hold returns. Out of the 43 Country specific MSCI indices we analyzed, half had more than a 10% chance of giving negative returns to buy-and-hold investors. India had a 6% chance (The Buy and Hold Bet.)

No company lasts forever. No market will always remain the best one to be in. No investment strategy will always deliver market-beating returns. No investor can consistently beat the market year-in/year-out.

No investment is forever.

Asian Paints?