Hello!

Hello!

Our backgrounds and how it shaped our thinking about systematic strategies.

Hi there! Thank you for subscribing to Free Float. In the weeks to come, we will be discussing a variety of systematic investment and allocation strategies, and how they fit into different investment goals. To kick things off, here’s a brief note from both of us.

Kishan

“Someone is sitting in the shade today because someone planted a tree a long time ago” - Warren Buffett

‘Everyone has a plan till they get hit in the face’ - Mike Tyson

When someone starts investing, one should ask themselves why are they investing? There is no wrong answer really, if one can afford to, speculating in markets can be a lot of fun. Trying to find the next Infosys, can one of most thrilling intellectual challenge and finding and capitalizing on one, can be a genius move compared to grandmaster’s and rewarding as well.

However, most people think that investing in markets is a “get-rich-quick” scheme. So they end up investing in a random stock or mutual fund, based on a recommendation or gut and sometimes it works or does not. Flailing about randomly, they pay a price in both time and money.

Every person is different, everyone has different financial circumstances, behavioral bias, and goals. It is important to build a pre-defined strategy relevant to that individual. If someone is naturally risk averse and does not need to take great amount of risk to achieve his financial goal, like he can invest 100% in postal savings and get there, he should do that. If someone has an above average risk profile and has most of his material needs taken care of and he wants to be aggressive, he should. If someone wants to be conservative and provide for his important needs first and then maybe, try to find the next Infosys with a smaller amount - an amount that he wont lose sleep over if he loses it - then that’s sensible thing to do.

Having an investment plan draws boundary lines based on investing objectives and constraints that helps guide an investor without losing her head during good or bad times.

Another reason to have pre-defined investment strategy is to minimize costs. Costs can be implicit or explicit, explicit costs can be transaction costs and investment losses. Implicit costs are opportunity costs. Keeping an eye on these costs allows someone to get closer to their goals. Or those costs put one further away.

One objective of investing is to benefit from snowball effect, which is when you roll down snow down a hill it starts out small but as it proceeds downwards and gathers momentum, the snowball gets larger and larger. This in investing happens through compounding. It is what Warren Buffet calls the eight wonder of the world; costs diminish compounding.

Why does someone abandon a strategy? Its due to disruption, like major change in finances or markets, that makes someone either more risk averse or more risk prone. It gets heady in this game and instead of taking a calibrated approach to the new circumstances, people lose perspective. The other reason is fatigue, people make plans all the time but rarely follow them. Especially a plan that involves sacrifice of spending, putting off today’s gratification to invest for the future and sticking to it for long term. It’s understandable.

Shyam

All active investing is market timing. All investing is active. You are not owed a return just because you took a risk.

To me, investing is really about managing risk and surviving long enough for market returns to compound and work its magic. Most investors focus only on one side of this equation: returns. But it is risk that takes them out of the market and interferes with the compounding.

The goal of every investment strategy is to maximize returns for the given amount of risk taken. And our responsibility as investors is to make sure that we enter into investments having fully understood the risks involved. After all, compounding cuts both ways.

The appeal of systematic investment strategies is that it gives us a standard framework to think through a given course of action. It helps us figure out if it is worth the effort after factoring in transaction costs and taxes. It helps us in answering questions of feasibility with respect to capacity, liquidity and impact. And more importantly, it keeps us honest.

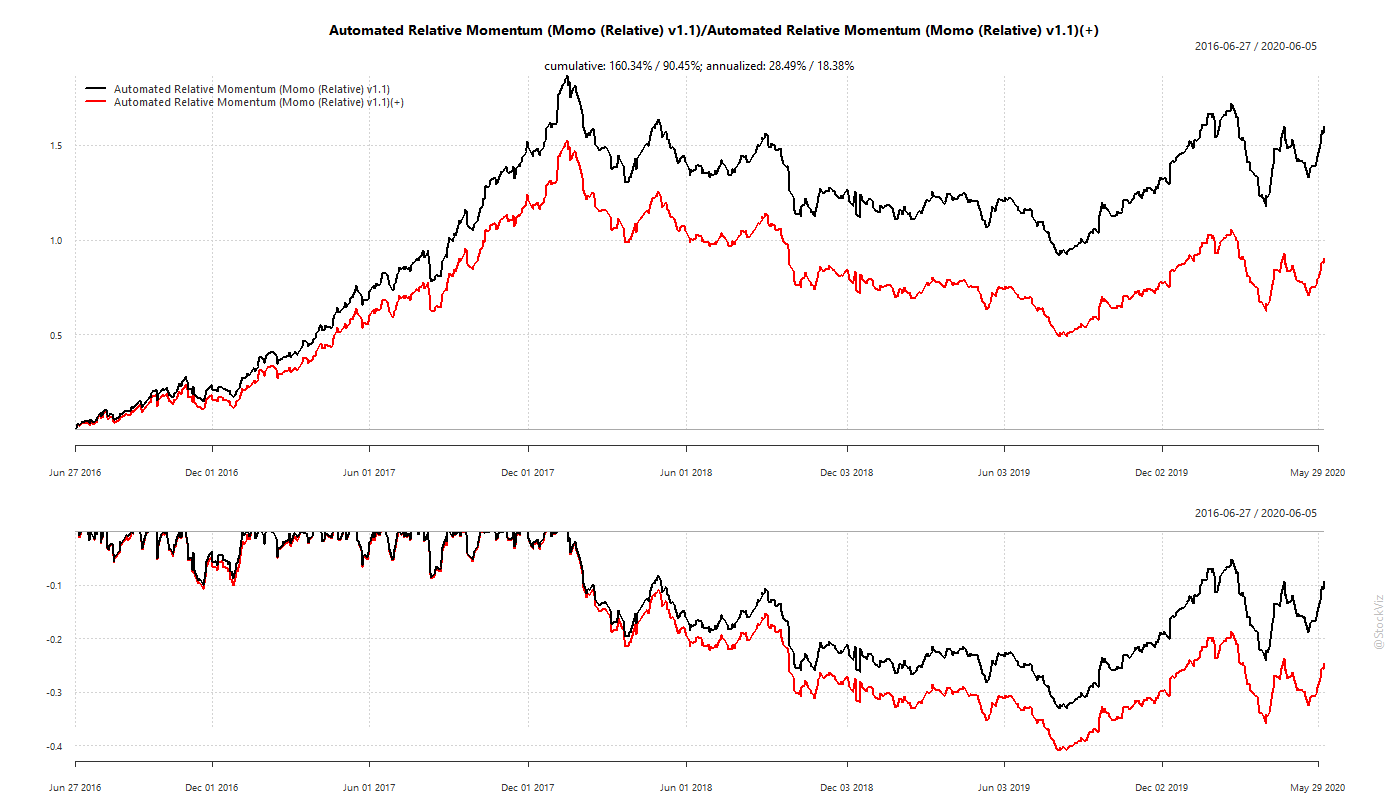

Subsequent posts in this newsletter will discuss different investment and allocation strategies. We will be posting cumulative return (sometimes called the equity curve) and drawdown charts that includes both gross (before transaction costs and STT) and net returns. Here’s a sample that also highlights the role of Securities Transaction Tax (STT) on returns:

Gross returns (black line) of 28.49% translates into net returns (red line) of 18.38% because of taxes. While most investors (and advisors) focus on the black line, it is the red one that should matter to you. So, if there is one thing that you should take away from our first letter, it is to always ask for the after-tax and transaction cost equity curve of any strategy put in front of you.